The Mega Backdoor Roth:

A Powerful Strategy for High Earners

If you're already maxing out your 401(k) and are still looking for more ways to build tax-free retirement wealth, the Mega Backdoor Roth might be the most powerful strategy you've never heard of. It's not available to everyone, and it does require a specific type of 401(k) plan, but for those who have access to it, it can unlock a significant amount of additional Roth savings each year.

Let me walk you through what it is, how it works, and why it's worth paying attention to.

What Is the Mega Backdoor Roth?

The MegaBackdoor Roth is not a separate account type. It's a strategy that allows certain individuals to contribute after-tax dollars to their employer-sponsored 401(k) plan and then convert those contributions into a Roth account, either a Roth 401(k) inside the plan, or a Roth IRA. (Fidelity, 2026)

The name says it all. It's like the Backdoor Roth IRA, but much bigger. While the regular Backdoor Roth IRA is capped at $7,000 per year(2025) subject to catch up contributions, the Mega Backdoor Roth can allow you to move significantly more into a Roth account in a single year, depending on your plan and how much room you have under the IRS limits.

Who Can Use It?

The Mega Backdoor Roth is designed for individuals who: (Fidelity, 2026)

• Are enrolled in an employer-sponsored 401(k) plan that allows after-tax contributions

• Have a plan that permits in-service withdrawals to a Roth IRA, or in-plan Roth conversions to a Roth 401(k)

• Have already maxed out their standard pre-tax or Roth 401(k) contributions and are looking to save even more

This strategy is most commonly available through larger employer plans. If you're not sure whether your plan allows it, check your Summary Plan Description or reach out to your HR department or plan administrator.

It's also worth noting that even if your income is too high to contribute directly to aRoth IRA, the Mega Backdoor Roth has no income limits.

How It Works: Step by Step

Step 1: Max Out Your Standard 401(k) Contribution

For 2025, the employee contribution limit for a 401(k) is $23,500 (or $31,000 if you're age 50 or older). This can be made as pre-tax or Roth contributions. (IRS, 2026)

Step 2: Make After-Tax Contributions

Once you'vehit the standard employee contribution limit, you may be able to continue contributing to your 401(k) on an after-tax basis, up to the IRS Section 415(c)overall plan limit. For 2025, that limit is $70,000 total, which includes your contributions, your employer's match, and any after-tax contributions. (Empower, 2026)

Step 3: Convert to a Roth Account

After making your after-tax contributions, you convert them to a Roth account, either through an in-plan Roth conversion to a Roth 401(k), or by rolling the funds out to a Roth IRA while still employed (if your plan allows in-service distributions). Since the money was already contributed after-tax, the conversion is generally tax-free, as long as you convert before any significant earnings accumulate. (Fidelity, 2026)

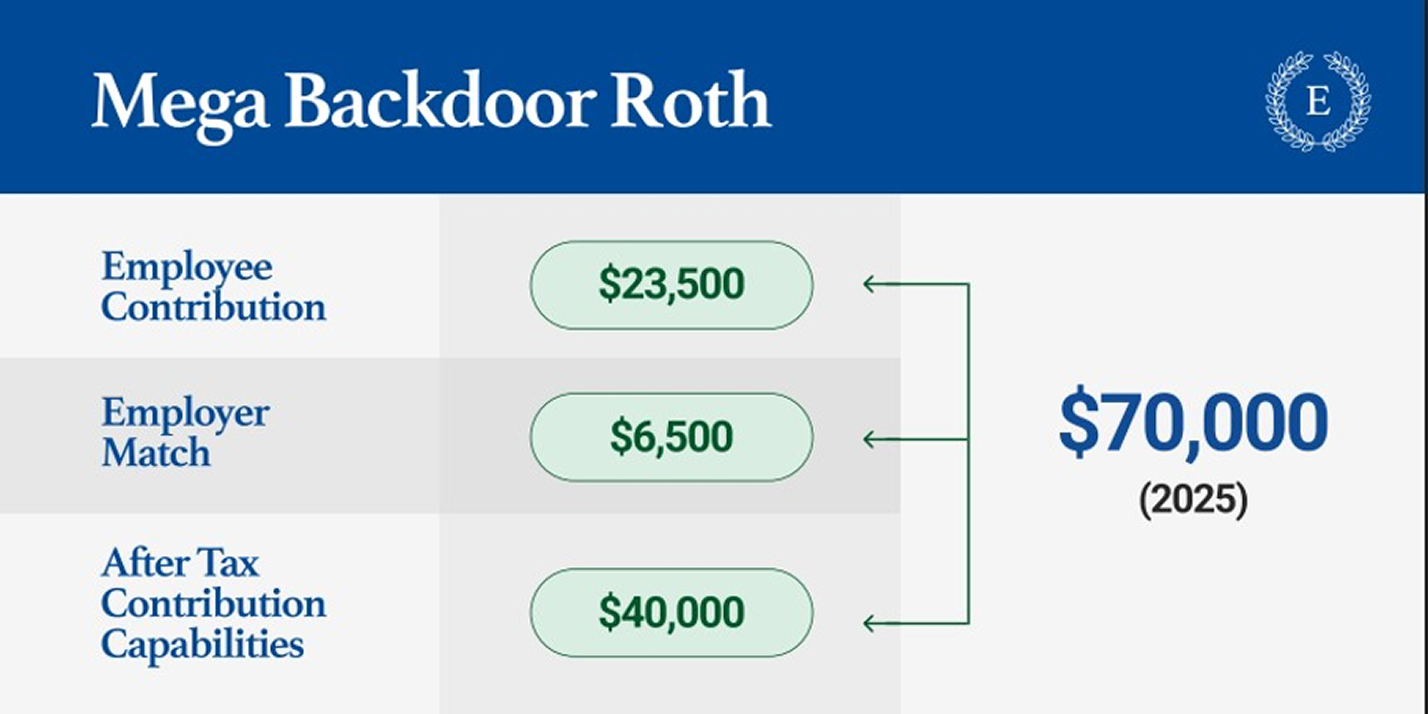

Breaking Down the Numbers (2025)

Here’s a simple example of how the contribution limits stack up for an employee under the age of 50 in 2025:

Note: Employer match amounts vary by plan and the $6,500 was just used for this example. The employee contribution amount can consist of both Pre-Tax and/orRoth monies but cannot go over the allowable aggregate total. The after-tax contribution capacity is the remaining room under the $70,000 total limit after accounting for employee and employer contributions.

Important Things to Consider

Your Plan Has to Allow It

Not every401(k) plan offers after-tax contributions or in-plan Roth conversion options.This is the first and most important box to check. Even if your employer offers a 401(k), the plan may not have the specific features needed to execute this strategy. Review your Summary Plan Description or ask your plan administrator directly.

Convert Quickly to Minimize Taxes

Any earnings that accumulate in the after-tax bucket before you convert them are taxable at conversion. The longer you wait to convert, the more potential tax exposure you have on those gains. If your plan allows it, converting frequently, or taking advantage of an automatic Roth sweep feature (if your plan has this feature), keeps the taxable earnings minimal. (Fidelity, 2026)

This Is Separate From the Backdoor Roth IRA

If you're already using the Backdoor Roth IRA strategy through a Traditional IRA conversion, that's a separate limit. You can potentially use both strategies in the same tax year. (District Capital Management, 2026)

ACP Testing Considerations

After-tax contributions from highly compensated employees are subject to ACP (ActualContribution Percentage) nondiscrimination testing. In some cases, if rank-and-file employees aren't contributing enough, after-tax contributions from high earners could be partially refunded, which can disrupt the strategy. (District Capital Management, 2026)

Why It Matters for High Earners

For 2025, Roth IRA contributions phase out completely for single filers above $165,000 in modified adjusted gross income (MAGI), and for married couples filing jointly above $246,000. The Backdoor Roth IRA solves part of that problem, but it's limited to $7,000 per year. (IRS, 2026)

The Mega Backdoor Roth can potentially allow tens of thousands of dollars more to flow into a Roth account in a single year. That's a meaningful difference for someone trying to build tax-free retirement income, especially over a long-time horizon where that money has the chance to grow.

Like all Roth money, once it's in, it grows tax-free, and qualified distributions in retirement are tax-free as well.

The Bottom Line

The Mega Backdoor Roth is one of the most powerful retirement savings tools available, but it comes with real complexity. It requires the right plan, careful execution, and coordination with your financial and tax professional to make sure it's done correctly. If you have access to it and the cash flow to take advantage of it, it may be worth considering.

Have questions about whether the Mega Backdoor Roth makes sense for your situation? Let's talk!

Disclaimer:This blog post is for educational purposes only and should not be construed as personalized financial or tax advice. Please consult with a qualified financial professional and/or tax advisor before making any decisions regarding 401(k) contributions, after-tax contributions, or Roth conversions. The availability of the Mega Backdoor Roth strategy depends on the specific features of your employer-sponsored retirement plan. After-tax contributions and in-plan Roth conversions may have tax implications depending on your individual circumstances. Exceeding IRS contribution limits may result in tax penalties and required corrections. This information is based on current IRS rules, which are subject to change. A Roth IRA conversion—sometimes called a backdoor Roth strategy—is a way to contribute to a Roth IRA when income exceeds standard limits. The converted amount is treated as taxable income and may affect your tax bracket. Federal, state, and local taxes may apply. If you’re required to take a minimum distribution in the year of conversion, it must be completed before converting. To qualify for tax-free withdrawals, you must generally be age 59½ and hold the converted funds in the Roth IRA for at least five years.Each conversion has its own five-year period, and early withdrawals may be subject to a 10% penalty unless an exception applies. Income limits still apply for future direct Roth IRA contributions. Contributions to a traditional IRA may be tax deductible in the contribution year, with current income tax due at withdrawal. Withdrawals prior to age 59 ½ may result in a 10% IRS penalty tax in addition to current income tax.